The impact of artificial intelligence and Industry 4.0 ontrans forming accounting and auditing practices

Abdulwahid Ahmad Hashed Abdullah a,1, Faozi A. Almaqtari b,*,2

a Department of Accounting, Prince Sattam Bin Abdulaziz University, Al-Kharj, Saudi Arabia

b Department of Accounting and Finance, College of Business Administration, A’Sharqiyah University (ASU), Ibra, Oman

2024/05/15 Ask help from Mr. Romi

Fig. 1 Got it.

Fig. 2 Which tables do the numbers in Fig. 2 come from? I want to find out.

- Yellow ones such as BIGD1 0.868, BIGD2 0.806, BIGD3 0.734 ->(1) Big Data

I know this comes from Table 4 Factor loading.

- Gray BigData -> Where do the AI numbers come from? AI->Ease of Use route number

I know this is the beta value from Table 8 SEM Estimation – Direct Effect Model.

-Q1. But where did AI 1.319 and Ease of USe 0.690 come from?

-Q2. Why are these numbers missing in fig.3?

Fig. 3 Which tables do the numbers in Fig. 3 come from? I want to find out.

-Q3. Why do yellow ones such as BIGD1 0.868 become 25.658 and BIGD2 0.806 become 19.829?

-Q4. What is the relationship between the following four tables and Fig. 3?

Table 8 SEM Estimation – Direct Effect Model.

Table 9 SEM Estimation – Indirect Effect Model - AI.

Table 10 SEM Estimation – Indirect Effect Model – AI Dimensions.

Table 11 SEM Estimation – Indirect Effect Model – Industry 4.0 readiness.

-Q5. about Table 5

It is said that 'Table 6 please Explain: diagonal elements are greater than the correlations between constructs for most cases, indicating good discriminant validity.' please explain it, thanks.

original [PDF] |

ABSTRACT

The main aim is to investigate the impact of artificial intelligence (AI), Industry 4.0 readiness, and Technology Acceptance Model (TAM) variables on various aspects of accounting and auditing operations. To evaluate the associations between the variables, the research design employs a mediation and path approach using SMART PLS. The study employs a convenience sampling method, which is augmented with snowball sampling. The sample size was determined using various techniques, yielding a final sample of 228 respondents. The findings indicate that leveraging AI, big data analytics, cloud computing, and deep learning advancements can improve accounting and auditing practices. AI technologies assist businesses in increasing their efficiency, accuracy, and decision-making capabilities, resulting in improved financial reporting and auditing processes. The study contributes to the theoretical explanation of the influence of AI adoption in accounting and auditing practices in the context of an emerging country, Saudi Arabia. The findings of the study have practical implications for accounting and auditing practitioners, policymakers, and scholars. The findings of this study can assist businesses in efficiently leveraging AI developments to improve their accounting and auditing operations. Policymakers can use the findings to create supporting frameworks and regulations that encourage the adoption and integration of artificial intelligence in the domain. These findings contribute to the existing stock of knowledge on the use of AI in accounting and auditing, as well as providing evidence of its benefits in the context of an emerging country.Introduction

Accounting and auditing are critical roles that ensure the reliability, credibility, and financial stability of a corporation. They provide objective assurance and contribute to market trust, making them essential to the overall health of the economy (Feliciano and Quick, 2022; Al-Hattami et al., 2021). Historically, these functions were mostly dependent on manual processes and human expertise. However, as information technology (IT) has grown, a paradigm shift in the way accounting and auditing are handled has occurred. Recognizing the relevance of IT in this context, organizations, accountants, auditors, professional bodies, academics, and regulators have switched their focus to improving auditing and accounting processes using technology (Al-Hattami, 2022; Al-Hattami, 2023).Curtis and Payne (2008) indicate that the use of technology, particularly information technology, has proven crucial for boosting audit quality and efficiency. It has a number of advantages, including enhanced dependability, productivity, efficiency, and decreased audit costs (Correia et al., 2020). The use of IT also saves time in audit tasks, which allows auditors to assign their efforts more effectively (Thottoli et al., 2022 ). Thus, the significant effect of technology on auditing is obvious, as it has become practically difficult to conduct an effective audit without embracing IT (Al-Hattami et al., 2021; Al-Hattami, 2021; Thottoli et al., 2022). Hence, with modern technologies such as Artificial Intelligence (AI) and Industry 4.0, the discipline of accounting and auditing has been developed tremendously (Jamwal et al., 2021; Enholm et al., 2022; Polak, 2021; Munoko et al., 2020; Han et al., 2023; Al-Sayyed et al., 2021). This has beenconfirmed by several studies (Lasi et al., 2014; Tjahjono et al., 2017; Jamwal et al., 2021; Loureiro et al., 2021; Enholm et al., 2022;Polak, 2021). Besides, technology integration in accounting procedures has also been identified as a technique to improve management control effectiveness (Al-Hattami and Kabra, 2022).

The rise of AI has significantly transformed the accounting profession, enhancing accuracy and data quality (Bin-Abbas and Bakry, 2014; Erasmus and Marnewick, 2021; Manita et al., 2020;Papagiannidis et al., 2022; Rezaee et al., 2018; Rushinek and Rushinek, 1989; Tsai et al., 2015; Willson and Pollard, 2009). Flowerday et al. (2006) , Sledgia nowski et al. (2017) , Tiberius and Hirth (2019) reported that the new challenges that are becoming more prevalent necessitate innovation in accounting practices. Key links to innovation include automation of routine tasks, improved accuracy, real-time reporting, data analytics, cybersecurity challenges, continuous learning, ethical considerations, global standardization, and emerging roles (Baldwin et al., 2006; Curtis and Payne, 2014; Tiberius and Hirth, 2019). In this context, accounting firms can efficiently utilize AI by automating repetitive tasks, implementing predictive analytics, incorporating AI tools, auditing procedures, blockchain technology, and AI-powered chatbots. Therefore, accounting practices can improve efficiency, accuracy, and strategic decision-making through modern technologies and leveraging Industry 4.0 capabilities (Burritt and Christ, 2016; Cervone, 2017; Di Vaio et al., 2020; Ghobakhloo, 2018; Sirisomboonsuk et al., 2018).

From the argument above, it is obvious that technology, particularly AI (Munoko et al., 2020; Han et al., 2023; Al-Sayyed et al., 2021; Zhang et al., 2020) and Industry 4.0 (Tavares et al., 2022; Fül ̈ op et al., 2022; ̈ Ozcan and Akkaya, 2020), have significantly impacted accounting and auditing worldwide. The use of thesetechnologies has become critical to the efficacy and efficiency of accounting and auditing operations. Studies (i.e., ACCA, 2019; Curtis and Payne, 2008; Correia et al., 2020; Thottoli et al., 2022 ) support the view that IT has the potential to improve audit quality, dependability, productivity, cost reduction, and time savings on audit duties. Besides, the integration of AI, machine learning, deep learning, big data analytics, data mining, and cloud computing into accounting and auditing processes enables the analysis of large volumes of financial data, the identification of patterns, trends, and anomalies, and improved decision-making (Coman et al., 2022; Lehner et al., 2022; Yoon, 2020).

While the use of technology in accounting and auditing has been extensively researched in developed countries, research in developing countries, such as Saudi Arabia, is scarce (Al-Hattami et al., 2021; Al-Mohammedi, 2020). For example, China’s Industry 4.0 development is heavily reliant on the integration of Industry 4.0 and improved artificial intelligence performance. Furthermore, the development of China’s Industry 4.0 is dependent on delivering a high level of artificial intelligence, the requisite financial resources, the formation of high level and advanced industrial zones, the enhancement of production processes, and research collaborations. As a result, advanced Industry 4.0 with smart production is achieved (Hou et al., 2020).

Saudi Arabia has made significant investments in new technologies such as artificial intelligence, 5 G, and data management(Alanazi, 2023; Ghazwani et al., 2022; Khan et al., 2022). These investments have aided the country’s position as a leader in these cutting-edge industries, promoting economic growth. Technology is also a crucial and key topic in Saudi Arabia’s Vision 2030, with digital transformation plans multiplying in recent years (Hassan, 2020; Alanazi, 2023; Dhar Dwivedi et al., 2021). The Saudi government also places emphasis on cybersecurity, coding, artificial intelligence, and gaming (Sairete et al., 2021 ). Ac cording to Sairete et al. (2021) , the PwC consulting firm, the world’s second-largest professional services network, AI might contribute $135 billion, or 12.4%, to Saudi Arabia’s GDP by 2030. One of the funda mental themes of the Saudi Vision 2030 is that AI has created a pool of opportunity for digital transformation and creative services. Thus, there are notable governmental efforts in Saudi Arabia toward digital transformation; however, the readiness of Saudi businesses for this digital transformation needs to be explored in terms of the factors influencing their readiness and the potential challenges that may arise. To that end, the purpose of this study is to fill a research gap in the literature. As a result, the purpose of this research is to investigate the impact of AI and Industry 4.0 readiness on accounting and auditing processes in Saudi Arabia. This research intends to provide significant insights into the factors, obstacles, and benefits of adopting and employing technology in accounting and auditing in the country by focusing on the specific context of Saudi Arabia.

This research contributes to the audit literature by addressing some research gaps. First, it is one of the first studies to study the factors influencing the intention to adopt and use emerging audit technology in Saudi Arabia, bringing insights to the setting of a developing country. This study broadens our understanding of the adoptionand utilization of emerging technologies by taking into account the country-specific factors at play by focusing on Saudi Arabia. Second, this study adds to our understanding of the factors that influence the adoption and use of developing audit technology. This study contributes to our under standing of the critical elements driving the adoption of these technologies by developing and empirically testing a theoretical model. This study’s empirical evidence and insights can help practitioners, policymakers, and researchers in Saudi Arabia develop strategies and policies to promote the adoption and successful use of emerging technologies in accounting and auditing. Third, the current study incorporates the TAM model in order to evaluate the readiness and intention to use AI and Industry 4.0 readiness in accounting and auditing operations. Finally, the current study could serve as a paradigm for future research in merging nations, particularly those in the Gulf regionand Arab countries with comparable cultures and views.

The present research is structured as follows: The research hypotheses are developed in Section 2. Section 3 discusses the methodology. Section 4 provides the data analysis and discussion. Section 5 contains additional analysis. Section 6 discusses the results and highlights the research implications, and section 7 summarizes the result and discusses the study’s limitations as well as future research.

Research model and hypothesis development

Technology acceptance model

The first Technology Acceptance Model (TAM) was proposed by Davis et al. (1989). The model has been regularly employed by re searchers to assess the users’ acceptability of information technologies (IT) (Usman et al., 2022; Qasim, Kharbat, 2020; Pedrosa et al., 2020; V ̆ arzaru, 2022). The model is characterised by its ease of use and perceived usefulness: two variables that influence users’ intention to use IT systems. Previous literature indicates that this model is a well-recognised model, which has been widely acknowledged to provide insights into the level of acceptance and adoption of IT systems (King & He, 2006; Usman et al., 2022 ; V ̆ arzaru, 2022). In addition, TAM is established as a simple model that captures the professionals’ behaviour and experience of IT use and implementation (Gefen, Karahanna, & Straub, 2003). It is built on the premise that professionals’ behaviour and experience in IT adoption drives IT implementation and use, which is also affected by practitioners’ perceived ease of use and usefulness. However, it may overlook other factors that influence user behavior, such as individual characteristics, experiences, and motivations. TAM assumes a static nature, implying that user perceptions remain consistent over time, but attitudes and beliefs may change as individuals acquire experience or the technology evolves (Muthia & Siti, 2023). It also does not account for extrinsic variables like social characteristics or organizational culture, limiting its explanatory ability in complex real-world scenarios (Muthia & Siti, 2023; Tulasi, 2022). It focuses on behavioral intention rather than actual behavior, and does not account for reverse causation or bidirectional interactions (Bara’ah et al., 2022; Meiryani et al., 2021). It also overemphasizes rational decision-making, assuming consumers make rational choices based on ease of use and utility (Malatji et al., 2020).

According to Ferri et al. (2021b), perceived ease of use and perceived usefulness are the two motivationalelements driving IT usage intention.

perceived utility reflects a person’s expectation of how a new IT system would boost their work performance. The second element, perceived ease of use, is an individual ’s perception of the effort involved in adopting a new workpattern (Ferri et al., 2021a). It also relatesto users’ perceptions of the benefits provided by a specific technology (Granic ́, Marangunic ́, 2019). In this sense,the TAM model’s perceived usefulness plays an important role in understandinguser behavior and desire to use technology (Davis, 1989). Interestingly, usefulness of a technology is influenced by its simplicity of use (Davis, 1989; Davis et al., 1989 ; Venkatesh et al., 2003). Pedrosa et al. (2020) validated this association between the two elements in a study on the drivers of computer-assisted auditing tools (CAATs) utilization among statutory auditors in a European country.

IT perceived usefulness is also a crucial element influencing its acceptance in several businesses, including auditing (Pedrosa et al., 2020). Research found that if a technologyoffers high benefits, users are more likely to favor it over alternative applications (Davis, 1989; Mei and Aun, 2019; Dharma et al., 2017; Al-Okaily, 2022; Thottoli et al., 2022). Pedrosa et al. (2020) and Dharma et al. (2017) also indicate that perceived benefit has a significant effect on IT audit adoption, which supports the argument of the effect of technology benefits on its acceptability. As a result, if a technology is seen to be lacking benefits, it is unlikely to be adopted (Mei and Aun, 2019), which explains why IT audit adoption can improve the audit profession and practices (Dowling, 2009; Thottoli & Thomas, 2022; Purnamasari et al., 2022; Pedrosa et al., 2020). On the otherhand, several researchers have found that perceived benefits have a marginal effect on IT audit adoption, e.g. (Kim et al., 2016).

Although many studies used this model to investigate technological acceptability in accounting and auditing (Venkatesh and Bala, 2008; V ̆ arzaru, 2022; Alshurafat et al., 2021; Ferri et al., 2021a; Ferri et al., 2021b; Usman et al., 2022; Qasim, Kharbat, 2020; Pedrosa et al., 2020), very few explored the perceived usefulness and ease of use of AI and Industry 4.0 in auditing and accounting in developing nations. As a result, this study employs this model, which has been also followed by many prior studies, to assess the acceptance and use of a new IT (e.g., Siew et al., 2020; Thottoli & Thomas, 2022; Pedrosa et al., 2020). To this end, the current study investigates how the Technology Acceptance Model (TAM) mediates the impact of AI and Industry 4.0 on accounting and auditing practices. Based on this discussion, the hypotheses are formulated as follows:

H1.. Perceived usefulness and ease of use mediate the relationship between the intention to use AI and accounting and auditing practices in Saudi Arabia. This hypothesis can be further divided into the following subhypotheses:

H1a. . Perceived usefulness mediates the relationship between the intention to use AI and accounting and auditing practices in Saudi Arabia.

H1b. . Perceived ease of use mediates the relationship between the intention to use AI and accounting and auditing practices in Saudi Arabia.

H2. . Perceived usefulness and ease of use mediate the relationship between the intention to use Industry 4.0 and accounting and auditing practices in Saudi Arabia. Based on this hypothesis, following sub-hypotheses are framed:

H2a. . Perceived usefulness mediates the relationship between the intention to use Industry 4.0 and accounting and auditing practices in Saudi Arabia.

H2b. . Perceived ease of use mediates the relationship between the intention to use Industry 4.0 and accounting and auditing practices in Saudi Arabia.

The effect of AI

The role of artificialintelligence (AI) in business operations has been extensively studied and recognized for its significant impact across various domains (Dhamija & Bag, 2020). One such domain where AI has shown potential is talent acquisition, and its adoption can be influenced by factors such as task-technology fit (Dishaw & Strong, 1999). The alignment between tasks performed and AI technologycapabilities plays a crucial role in its acceptance. Additionally, understanding the adoption of AI-basedtechnologies in different contexts is important (Dhamija & Bag, 2020). As businesses use AI to reinvent processes and generate evidence-based data analysis, AI governance is critical for digital innovation (Papagiannidis et al., 2022 ). Singapore leads the area in AI experimentation across multiple industries, whereas Malaysia is gradually using AI in accordance with the TN50 and IR 4.0. Early adopters such as Singapore, Malaysia, Vietnam, Indonesia, the Philippines, and Thailand might obtain a competitive advantage by adopting AI as a potential revenue source, however ASEAN countries such as Cambodia, Myanmar, Brunei, and Laos have low adoption (Mohd Noor and Mansor, 2019). Thus, research is crucial in aligning theory and practice in auditing, with some leading firms integrating big data into their practices (Gepp et al., 2018; Schmitz and Leoni, 2019).

AI has brought forth various benefits and transformations in the accounting profession. It can automate monotonous procedures, simplify data analysis, make better decisions, and streamline auditing processes (Dhamija & Bag, 2020). The adoption of technology, specifically artificial intelligence (AI) (Munoko et al., 2020; Han et al., 2023; Al-Sayyed et al., 2021; Zhang et al., 2020 ), and Industry 4.0 (Tavares et al., 2022; Fül ̈ op et al., 2022; ̈ Ozcan and Akkaya, 2020), has had a significant impact on the field of accounting and auditing worldwide. Using AI including machine learning, deep learning, big data analytics, data mining, and cloud computing in accounting and auditing practices has leveraged the possibility of processing massive volumes of financial data, facilitating the identification of patterns, trends, and anomalies. Further, the use of AI in accounting and auditing has improved decision-making abilities (Coman et al., 2022;Lehner et al., 2022;Yoon, 2020).

AI has revolutionized accounting and auditing by automating common operations like data entry (V ̆ arzaru, 2022) and reconciliation (Shaffer et al., 2020), allowing accountants to focus on more challenging tasks (Munoko et al., 2020; V ̆ arzaru, 2022; Zhang et al., 2020 ). AI-powered automation solutions, such as robotic process automation (RPA) systems (Gotthardt et al., 2020; Losbichler and Lehner, 2021), extract (Sledgianowski et al., 2017 ), categorize (Issa et al., 2016; O’Leary, 2009; Sledgianowski et al., 2017 ), and enter data (V ̆ arzaru, 2022), enabling faster financial forecasting and identifying anomalies in financial records (Chen, 2021; Faccia et al., 2019; Losbichler and Lehner, 2021; Zhang et al., 2020 ). AI also improves decision-making by analyzing massive amounts of data (Gomez, 2018; Kopalle et al., 2022; Yoon, 2020) and discovering patterns in real-time (Sledgianowski et al., 2017; Sutton et al., 2016). Continuous auditing tools, developed by AI, allow real-time monitoring of financial activities (Sledgianowski et al., 2017; Sutton et al., 2016), reducing errors and enabling a more thorough evaluation of financial data (Faccia et al., 2019; V ̆arzaru, 2022). AI can predict future trends based on historical data (Gomez, 2018; Sutton et al., 2016), improve financial forecasting (Chen, 2021; Losbichler and Lehner, 2021), budgeting, and detect fraudulent transactions (Gepp et al., 2018; Sledgianowski et al., 2017; Yoon, 2020). Natural Language Processing (NLP) allows AI to analyze unstructured text (Munoko et al., 2020; Sun and Vasarhelyi, 2018; Tiberius and Hirth, 2019), improve compliance, and handle financial inquiries (Sun and Vasarhelyi, 2018). AI also automatically detects transactions that violate regulatory standards, reducing noncompliance risks (Gepp et al., 2018; Sledgianowski et al., 2017). Robotic Process Automation (RPA) systems can automate regular bookkeeping activities (Earley, 2015; Faccia et al., 2019), minimising the need for human involvement (Gotthardt et al., 2020; O’Leary, 2009). AI algorithms can also rapidly analyse big datasets (Brown-Liburd and Vasarhelyi, 2015; Cockcroft and Russell, 2018; Salijeni et al., 2019), detecting patterns, trends, and abnormalities (Gomez, 2018; Kopalle et al., 2022; Sledgianowski et al., 2017; Sutton et al., 2016; Yoon, 2020). This allows auditors to discover abnormalities or patterns that may indicate fraud (Gomez, 2018; Kopalle et al., 2022; Yoon, 2020).

AI algorithms can automate typical accounting processes like data entry and transaction processing, saving time and decreasing human error (Dhamija & Bag, 2020; Handoko, 2021). Besides, AI systems can assess massive amounts of financial data quickly and efficiently, assisting in the detection of patterns, anomalies, and trends that people may miss (Dhamija & Bag, 2020; Coman et al., 2022). This enhanced data analysis capability also aids in the detection and evaluation of fraud (Dhamija & Bag, 2020). Better decision-making has also emerged from the use of AI in accounting and auditing because AI can provide realtime insights and predictive analytics, helping accountants and audi tors to make more informed decisions (Dhamija & Bag, 2020). It can help with financial forecasting and scenario analysis, producing reliable financial predictions (Coman et al., 2012). In addition, AI can enhance audit efficiency and effectiveness by assessing financial statements, identifying potential hazards, and recommending areas for additional examination (Dhamija & Bag, 2020).

While AI technology has many advantages, it is crucial to note that it is not intended to replace human accountants and auditors but rather to supplement their talents (Dhamija & Bag, 2020). Thus, human judgment and decision-making are still critical (Coman et al., 2022; Yoon, 2020). The incorporation of AI in accounting processes necessitates the development of new abilitiesand the adaptationto shifting responsibilities for accountants and auditors (Coman et al., 2022). They need to become proficient in utilizing AI tools, interpreting AI-generated insights, and understanding the limitations and ethical considerations associated with AI technologies (Coman et al., 2022; Lehner et al., 2022). Thus, the following hypothesis is developed:

H3. . The usageof AI has a positiveeffect on accounting and auditing practices in Saudi Arabia.

The effect of Industry 4.0

Several studies have investigated the role of Industry 4.0 in different contexts (Burritt and Christ, 2016; Ghobakhloo, 2020; Kamble et al., 2018; Kiel et al., 2017; Masood and Sonntag, 2020; Müller et al., 2018; Nascimento et al., 2019; Stock and Seliger, 2016). While some studies investigate the readiness to adopt Industry 4.0 (Masood and Sonntag, 2020; Schumacher et al., 2016),some studies investigate the challenges, opportunities, and benefits of Industry 4.0 (Alaloul et al., 2020; Ghobakhloo, 2020, 2020; Ivanov et al., 2021; Kiel et al., 2017; Masood and Sonntag, 2020; Müller et al., 2018; Stock and Seliger, 2016). Recently, the focus on Industry 4.0 is on the enhancement of the performance by reducing errors, increase product quality, freeing humans from menial and/or dangerous tasks and providing consumers with the products they desire at times when they desire them (Burritt and Christ, 2016). In the new Industry 4.0 paradigm, Boyer, Kokosy (2022) investigated how IT innovation tools might support collaborative governance. Boyer, Kokosy (2022) emphasises how complex interactions among actors can spark fresh ideas and successfully implement Industry 4.0 advancements. This may necessitates integrating IT innovation tools and collaborative governance, which can effectively address Industry 4.0 concerns, stimulating creativity and resolving potential intergovernmental conflicts (Hwang, 2017).

China’s Industry 4.0 development is heavily reliant on the integration of Industry 4.0 and improved artificial intelligence performance. Furthermore, the development of China’s Industry 4.0 is dependent on delivering a high level of artificial intelligence, the requisite financial resources, the formation of high level and advanced industrial zones, the enhancement of production processes, and research collaborations. As a result, advanced Industry 4.0 with smart production is achieved (Hou et al., 2020). While there is a growing body of literature on AI’s po tential, there is a lack of comprehensivestudies covering all Industry 4.0 technologies, including the Internet of Things, big data analytics, and cloud computing. A comprehensive study linking these technologies to AI in accounting and auditing could help understand the synergies and challenges of these technologies in the financial sector. According, the current study hypothesize that:

H4. . Industry 4.0 readiness has a positive effect on accounting and auditing practices in Saudi Arabia.

Research design

Conceptual framework and research design

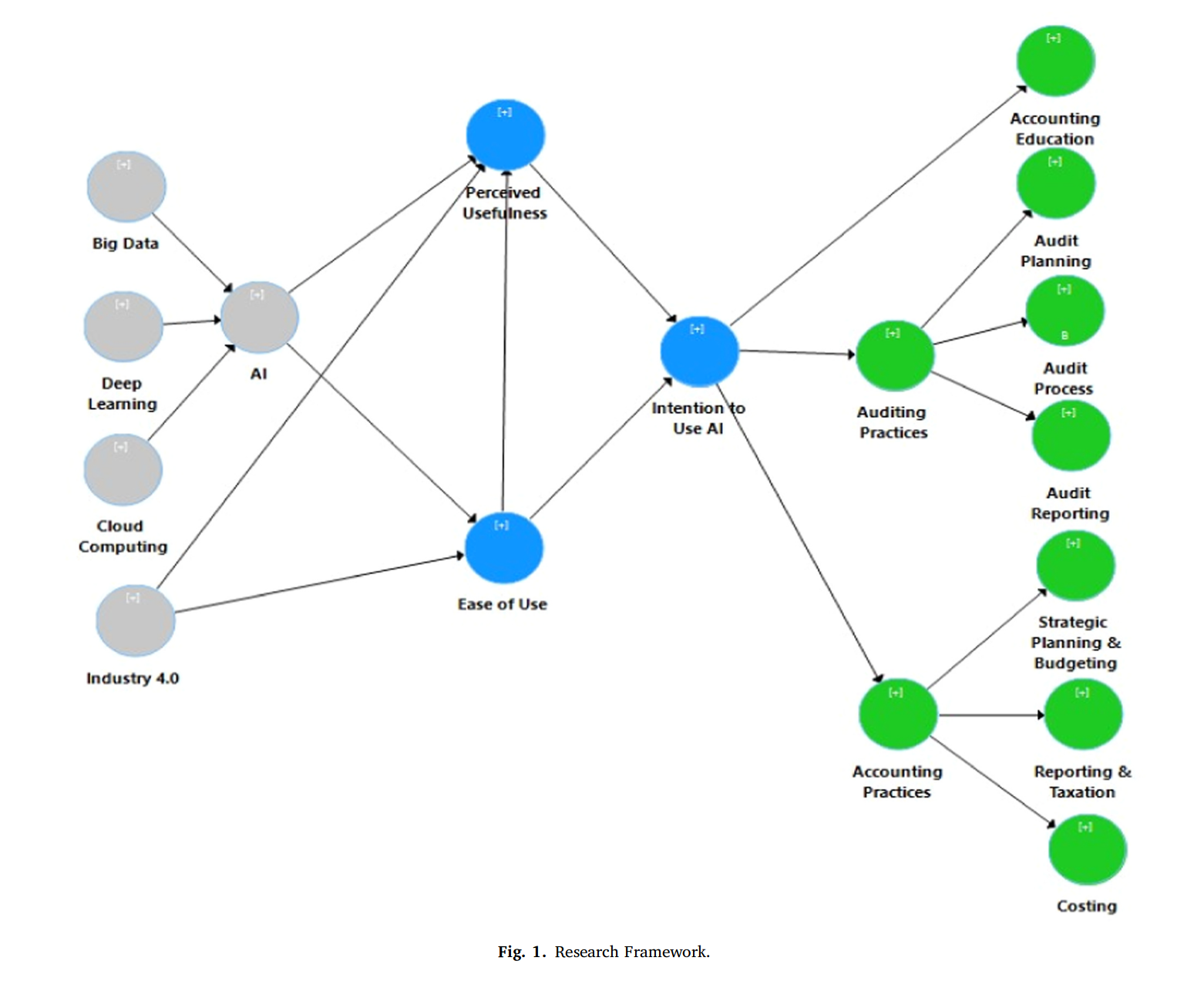

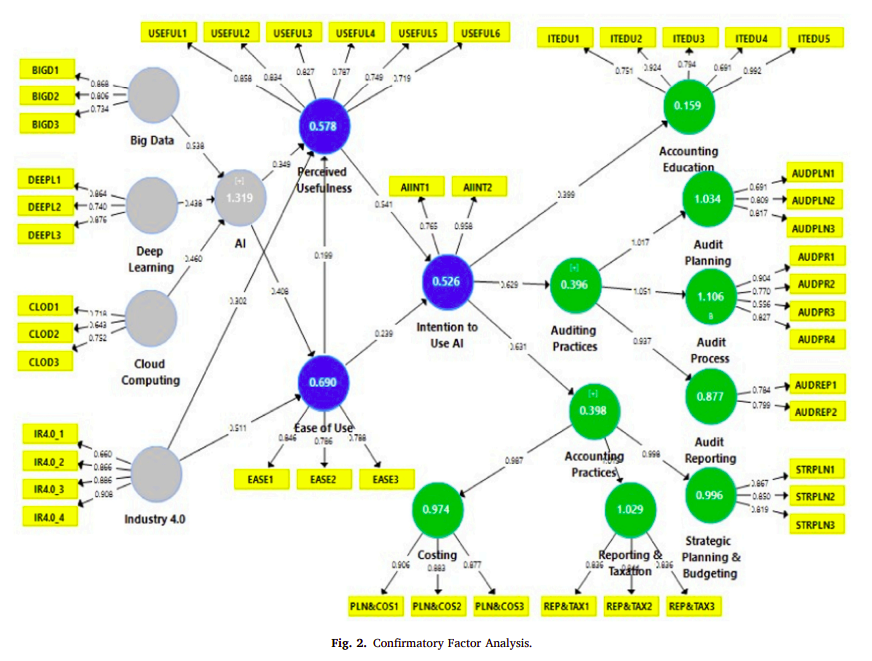

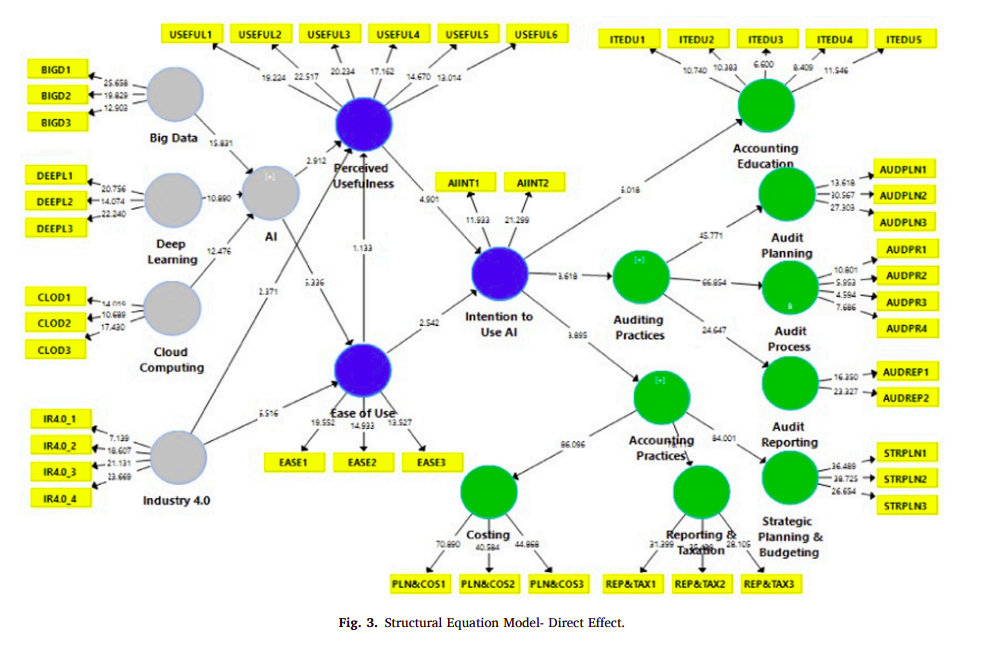

The research design outlined in Fig. 1 focuses on examining the influence of AI on accounting and auditing practices. The independent variables are AI (big data, deep learning, and cloud computing), Industry 4.0 readiness, and the Technology Acceptance Model (TAM) variables (ease of use, perceivedusefulness, and intention to use AI). The dependent variables pertain to various aspects of accounting and auditing practices, including accounting education, auditing practices (audit planning, audit process, and audit reporting), and accounting practices (strategic planning and budgeting, reporting and taxation, and costing). The study intends to investigate how AI, Industry4.0 readiness, and TAM components influence accounting and auditing practices by adding these variables into the research methodology.

The research model presents a mediation and path framework to evaluate the interactions between these factors. It implies that AI and Industry 4.0 readiness operate as predictors, influencing the intention to use AI in accounting and auditing practices. The aim to adoptIT, as well as the anticipatedbenefits, operate as meditators that influence the final output, which is accounting and auditing practices.

The inclusion of accounting and auditing practices as dependent variables allows a more in-depth evaluation of the influence of IT on different parts of these practices. Investigating how AI and Industry 4.0 readiness affect accounting education, for example, can provide insights into the evolving skill sets required of accountants in the digital era. Similarly, exploring the impact of AI and Industry 4.0 readiness on auditing practices, such as audit planning, process, and reporting, can shed light on the efficiency and effectiveness improvements brought about by the two technologies. Lastly, examining AI and Industry 4.0 readiness influence on accounting practices, including strategic planning and budgeting, reporting and taxation, and costing, can offer insights into how technology adoption affects financial management and decision-making processes.

Data and sample

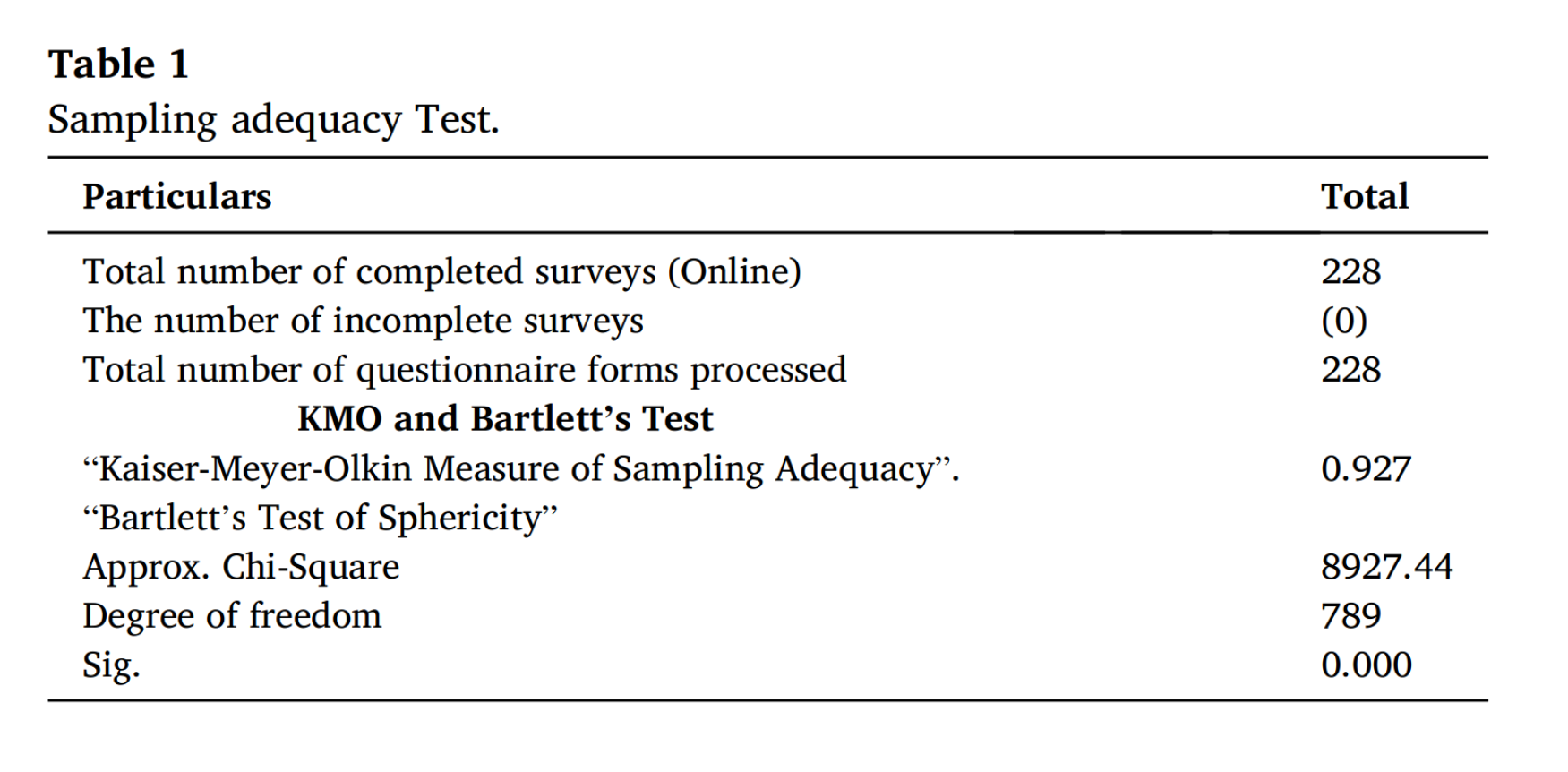

The population of the study consists of respondents from Saudi Arabia, which aligns with the research objective of examining the impact of AI and Industry 4.0 readiness on accounting and auditing practices in this context. The study employs a non-probability convenience sampling approach, as well as snowball sampling, which is justified by previous research suggesting their suitability for processing multivariate data and estimating results. The study used literature and previous research to estimate the sample size, based on assumed effect sizes relevant to the investigation. The researchers used established methods and standards from prior research studies by Bollen (1989), Christopher Westland (2010), and Long et al. (1990) to determine the minimal sample size required for the study. They calculated the sample size using free statistical software based on PLS path modelling, accounting for both latent and observable variables, effect magnitude, statistical power level, and probability level. The calculated sample size

yielded 148 participants. Other inputs included the desired level of confidence and statistical power, with a goal of achieving a confidence level of 95% to ensure the accuracy of the findings. In this regard, GPower software was used, which suggested a sample size of 163 re spondents. The actual data collection method, however, resulted in the collection of 228 surveys using an online questionnaire sent via Google Docs. To disseminate the survey and collect data, the researchers used several social media platforms such as Facebook, WhatsApp, and email. To enhance response rates and reduce low-quality responses, measures such as making all questions mandatory and utilizing respondentfriendly phrasing for closed-ended questions were implemented to assure thorough data. The researchers also used targeted distribution platforms with brief letters that emphasized brevity, which resulted in a 20% boost in response rate.

Finally, the study’s final sample size was determined to be 228 survey respondents, which were regarded statistically sufficient for pre dicting the outcomes. This conclusion is supported by the sampling and sample adequacy analyses presented in Table 1. The Kaiser-Meyer-Olkin Sampling Adequacy Measure returned a value greater than 0.7, which is considered satisfactory. Furthermore, the significance level for this test was quite high at 1%, indicatingthat the samplefit and was appropriate. With a value of 8927.44 and 789 degrees of freedom, Bartlett’s test also confirmed the sufficiency of the factor analysis.

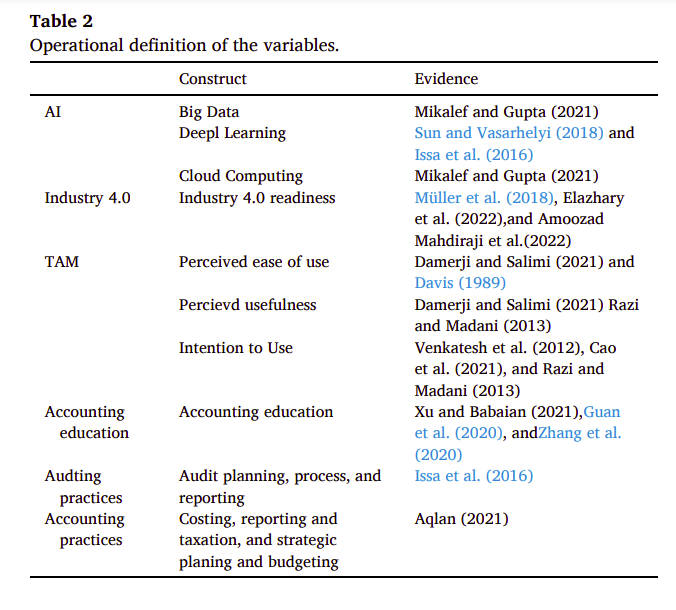

The current study used an online questionnaire survey to collect data from a variety of respondents, including external auditors, board members, CFOs, senior executives, internal auditors, and accountants from various Saudi organizations. The research instrument was developed based on relevant literature to ensure that it addressed all major topics related to the research objectives. The research instrument includes 58 items that were carefully constructed to represent each specific dimension of the current study. The items were developed to perceive respondents’ perceptions on the impact of AI and Industry 4.0 readiness on accounting and auditing processes in Saudi Arabia. All items included in the survey were constructed using a 5-point Likert scale. The scale ranges from 1 to 5. While1 indicates "strongly disagree", the scale of 5 represents"strongly agree." This enabled the researchers to investigate how much respondents agreed or disagreed with the statements of the survey. To ensure comprehensiveness, the questionnaire was structured into fourteen dimensions. These dimensions encompassed various aspects relevant to the research objectives, covering topics such as big data, deep learning, cloud computing, Industry 4.0 readiness, ease of use, perceived usefulness, intention to use AI, accounting education, audit planning, audit process, audit reporting, accounting strategic planning and budgeting, reporting and taxation, and costing. Table 2 provides the measurement scales synthesized from prior studies and Appendix I demonstrates the operational definition of the variables.

Empirical results

Demographic analysis of the sample

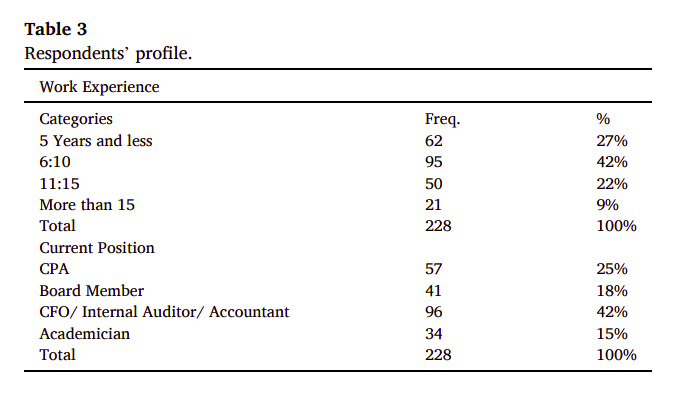

Table 3 provides an overview of the respondents’ profile in terms of their work experience and current positions. The findings indicate that among the participants, 27% had 5 years or less of work experience, while 42% had 6 to 10 years of experience. A total of 22% had 11 to 15 years of experience, and 9% had more than 15 years of experience. The majority of respondents (42%) worked as CFOs, internal auditors, or accountants in their current roles. CPAs made up 25% of the sample, board members made up 18%, and academics made up 15%.

Model’s measurement

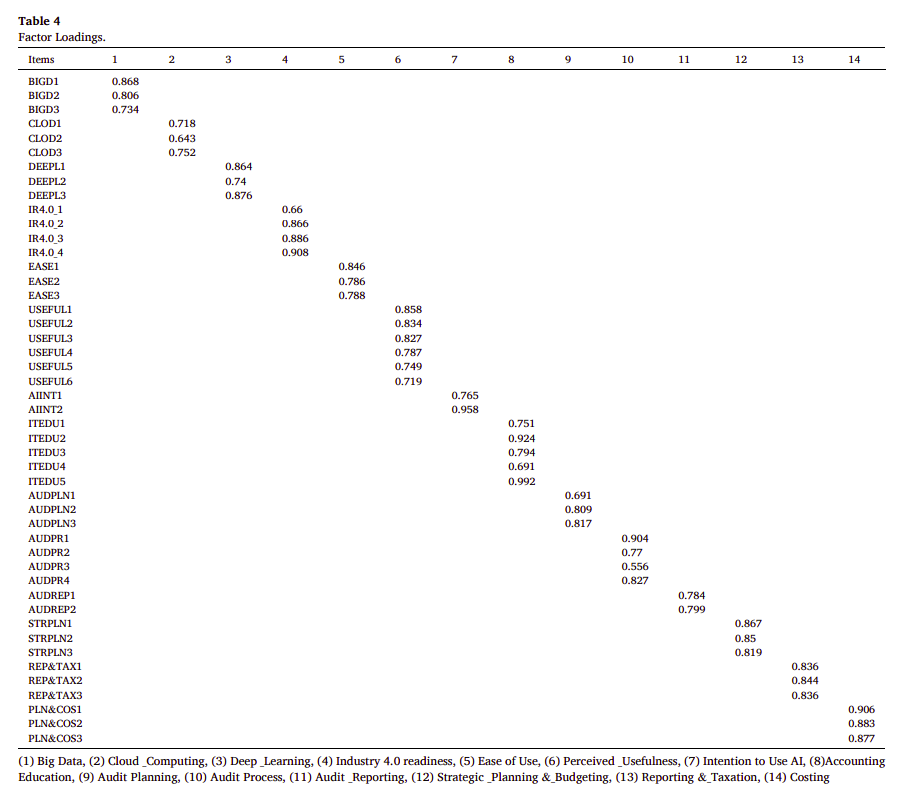

Factor loadings

(請看W04-參考資料的驗證性因素分析(Confirmatory Factor

Table 4 shows the results of the confirmatory factor analysis using Partial Least Squares (PLS). The findings reveal that the items used to measure each construct have high relationships with the structures they are measuring. The value of each item’s factor loadings exceeds the criterion threshold of 0.50, as proposed by Chin (2010). This shows a high level of convergent validity. The findings of the factor loadings show that the values range from 0.515 to 0.992, indicating a strong link between the items and their underlying constructs. The item factor loading values above the recommended threshold value (0.50) was suggested by Chin et al. (2008). For example, item AIINT2 exhibits a factor loading of 0.958, implying that it has a significant link with the construct “AI.” Similarly, items related to “Ease of Use” (EASE1, EASE2, EASE3) and “Strategic Planning & Budgeting” (STRPLN1, STRPLN2, STRPLN3) had factor loadings exceeding 0.75 suggest a strong shared variance with the latent constructs.

The factor loadings provide evidence for the convergent validity of the measurement model used in the study because they indicate that the items effectively measure their respective constructs and contribute significantly to the overall measurement model. Consequently, these findings enhance the reliability and validity of the study’s measurement instrument, as well. Fig. 2 also demonstrates the confirmatory factor analysis.

[Table 2]

[Table 3]

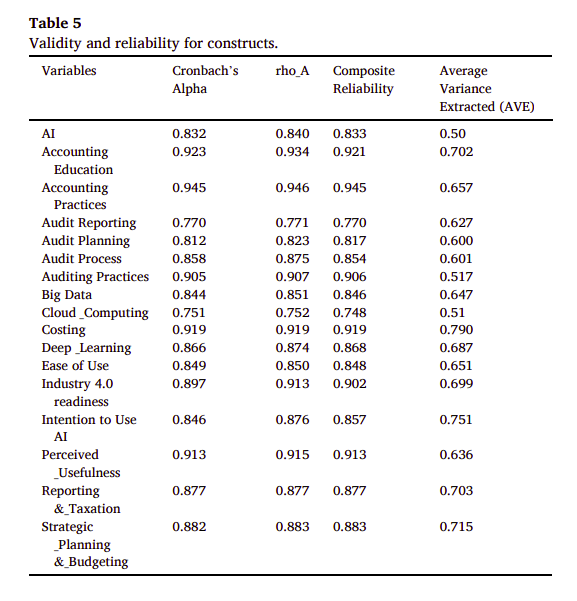

Validity and reliability

Table 5 displays the reliability and validity measures for each construct in the study. The findings show the indicators for Cronbach’s alpha, Rho_A, composite reliability, and average variance extracted (AVE). Cronbach’s alpha measures internal consistency reliability, which indicates how closely the items within a construct are related to each other. In this study, all constructs have Cronbach’s alpha values above 0.70, ranging from 0.770 to 0.945. These values suggest good internal consistency, indicating that the items within each construct are reliably measuring the same underlying concept. Furthermore, Rho_A, another measure of reliability, displays high values for all constructs, ranging from 0.771 to 0.946. These values add to the measurement items’ internal consistency.

Composite reliability assesses the construct’s dependability by considering both the items’ internal consistency and their intercorrelations. Like Cronbach’s alpha and Rho_A, composite reliability values greater than 0.70 imply high dependability. Since all constructs in this investigation have composite reliability values ranging from 0.748 to 0.945, there is strong dependability. Finally, the average variance extracted (AVE) evaluates the amount of variance captured by the construct in comparison to the measurement error. AVE values greater than 0.50 are generally regarded as satisfactory, suggesting that the measuring items explain more than half of the variance in the construct. All constructs in this investigation have AVE values greater than 0.50, ranging from 0.517 to 0.790, which shows that the constructs properly capture the underlying variance. Overall, the constructs in the study had high reliability and validity measures. Cronbach’s alpha, Rho_A, composite reliability, and AVE are all in the acceptable range, indicating good internal consistency, reliability, and convergent validity, which implies that the measuring items in the study exhibit reliability and validity in assessing their respective constructs.

[Table 4]

[Fig. 2]

[Table 5]

[Table 6]

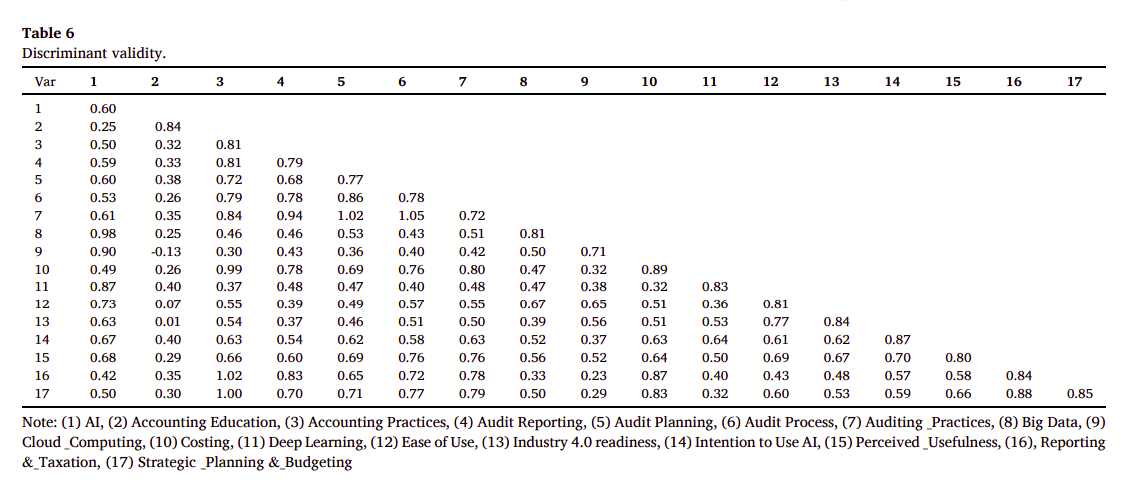

Discriminant validity

Table 6 shows the results of the discriminant validity analysis. We can observe that the diagonal elements are greater than the correlations between constructs for most cases, indicating good discriminant validity. The findings demonstrate strong correlation values among items that assess the same construct, indicating that these items accurately represent their respective construct and not any other construct. This observation is supported by the fact that the correlation values between each construct and other constructs are lower than the self-correlation values of the construct itself (Fornell and Larcker, 1981). Descriptive statistics

[Table 7]

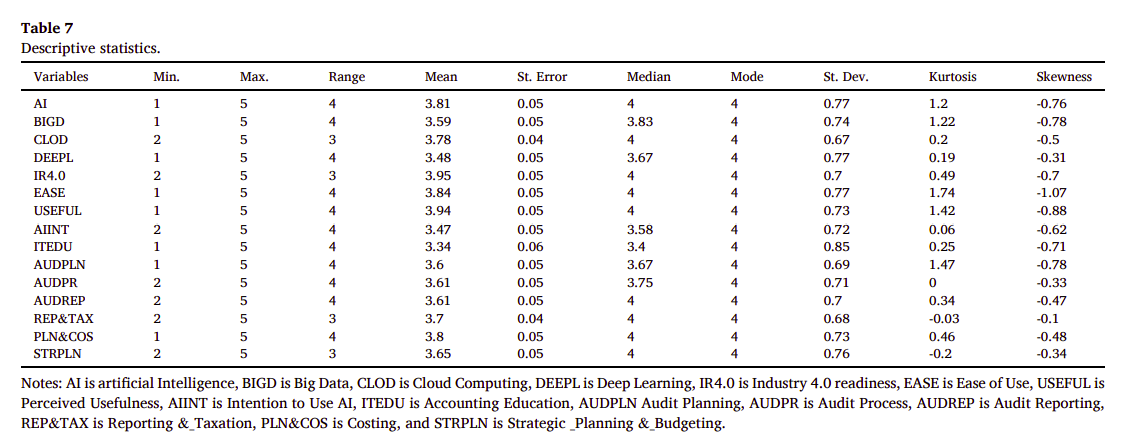

Table 7 provides descriptive statistics for the variables of the study. The results show that the range of the variables is 4, which is between a minimum value of 1 and a maximum value of 5 except for IR4.0, AIINT, AUDPR, AUDREP, REP&TAX, STRPLN that have a range value of 3 (Min. = 2 and Max. = 5). Further, the results indicate that the average values of the variables are about 4, indicating that the respondents perceived a positive perception of the statements asked. The results also show that the skewness and the kurtosis values are in the range of ( ± 1) for skewness and ( ± 3) for kurtosis, which indicate that the data is normally distributed.

Structural model

Fig. 3 displays the hypothesized or predicted structural approach for the current study variables. It provides the direct effect model as presented in Fig. 1.

Results estimation- direct effect

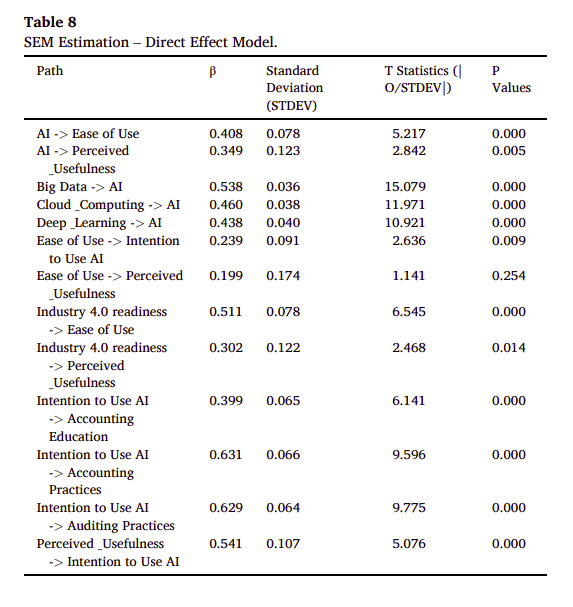

Table 8 provides the estimates of SEM analysis. The findings suggest a potential positive association between AI and perceived ease of use. A moderately strong positive coefficient (β + = 0.408) with a high level of significance (p = 0.001) reveals a possible influence of AI on Ease of Use. This tentative evidence suggests that AI technologies may be perceived as user-friendly and relatively simple to use in the context of accounting and auditing practices. Additionally, the study indicates a potential link between AI and the perceived usefulness of technology. A positive coefficient (β + = 0.349) and a highly significant connection (p = 0.005) tentatively support the idea that AI could be considered advantageous and valuable for enhancing accounting and auditing tasks in Saudi Arabia. This is consistent with several studies (e.g., Munoko et al., 2020; Han et al., 2023; Al-Sayyed et al., 2021; Zhang et al., 2020) that indicated that accounting and auditing practices are significantly affected by AI in different countries. Consistently, Correia et al. (2020) and Thottoli et al. (2022) indicated that the application of AI has become important to the efficacy and efficiency of accounting and auditing activities.

[Fig. 3]

[Table 8]

The results of the present study demonstrate that AI dimensions such as Big Data, Cloud Computing, and Deep Learning associates positively with AI acceptance and utilization. The effect of Big Data on AI acceptability is especially significant, with apositive coefficient (β + = 0.538) and high significance (p = 0.001). This robust relationship underscores the pivotal role of Big Data in fostering the adoption of AI in accounting and auditing practices. In the same context, a positive correlation (β + = 0.460) and a significant association (p = 0.001) support the influence of Cloud Computing on AI. This suggests that using cloudbased technology may be perceived as facilitating easier AI integration and implementation in the accounting and auditing arena. In addition, the results demonstrated a significant relation between Deep Learning and AI, evidenced by a positive coefficient (β + = 0.438) and a high level of significance (p = 0.001). This underscores the significance of advanced machine learning methodologies, such as Deep Learning, in enhancing the capabilities of AI for applications in accounting and auditing.

The study findings also emphasize the importance of perceived ease of use in affecting the intention to use AI. A positive coefficient (β + = 0.239) and a statistical significance (p = 0.009) support the influence of Ease of Use on Intention to Use AI, indicating that respondents who believe AI is simple to use are more likely to have a strong desire to adopt and apply AI technology in their professional operations. The study does, however, indicate a weak positive association between perceived ease of use and perceived usefulness of AI, as evidenced by a positive coefficient (β + = 0.199). However, the relationship is not statistically significant (p = 0.254).

The findings also show that Industry 4.0 readiness has a significant impact on AI’s perceived ease of use and usefulness. A moderately strong positive coefficient (β + = 0.511) and statistical significance (p = 0.001) support the effect of Industry 4.0 readiness on Ease of Use. Similarly, a positive coefficient (β + = 0.302) and statistical significance (p = 0.014) support the effect of Industry 4.0 readiness on perceived usefulness. This demonstrates the importance of Industry 4.0 readiness in impacting the usability and perceived value of AI in accounting and auditing operations.

The study found a link between the intention to use AI and accounting education, accounting processes, and auditing methods. A positive association (β + = 0.399) and significant effect (p = 0.001) support the effect of Intention to Use AI on Accounting Education. Similarly, large positive coefficients (β + = 0.631 and β + = 0.629, respectively) and high significance (p = 0.001) support the effect of Intention to Use AI on Accounting and Auditing Practices.

Results estimation- indirect effect

The effect of AI

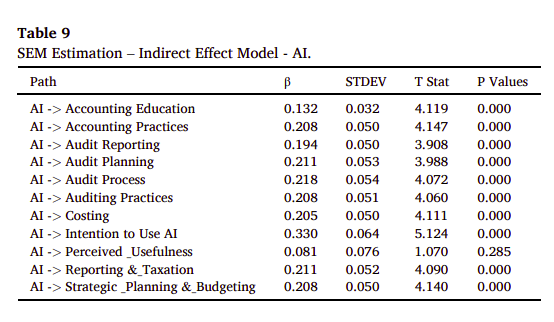

The results in Table 9 indicate a positive coefficient (β + = 0.132) and a significant relationship (p = 0.001) of the integration of AI in accounting education. It has been also found that AI positively influences accounting processes (AI -> Accounting procedures) with a coefficient (β + = 0.208) and a significant association (p = 0.001). This highlights AI’s ability to improve accounting systems by automating tasks, increasing data accuracy, and giving advanced analytical capabilities.

In addition, the results indicate that AI has a significant effect on audit reporting with (β + = 0.194) and a significant (p = 0.001), which support that AI can assist auditors in analyzing massive volumes of financial data, detecting anomalies, and improving audit report quality. Furthermore, AI has a significant impact on audit planning with (β + = 0.211) and a significant effect (p = 0.001), which means that by assessing prior data and offering applicable audit procedures, AI technology can help to enhance resource allocation and efficiency.

The present study also identified a positive relationship (p = 0.001) between AI and the total audit process (AI -> Audit Process) (β + = 0.218). This indicates that AI may automate certain audit operations, reducing manual errors and freeing up auditors to focus on higher-value duties, which increases efficiency and effectiveness.

In terms of general auditing procedures (AI -> Auditing procedures), AI has a positive coefficient (β + = 0.208) and a significant association (p = 0.001). This could mean that the integration of AI technologies can improve auditing procedures by automating data collection and analysis, increasing risk assessment, and providing valuable insights. In the same context, AI has a positive significant impact on costing (AI -> Costing), (β + = 0.205; p = 0.001 < 0.01). Organizations may improve cost management and decision-making by employing AI to optimize cost accounting processes, analyze production data, and identify cost drivers. Furthermore, exposure to AI has a positive and significant association on the intention to use AI (AI -> Intention to Use AI), (β + = 0.330; p = 0.001). Respondents perceive AI benefits like increased efficiency and accuracy, which leads to a stronger intention to implement AI into their professional operations.

Although the association between AI and perceived usefulness (AI -> Perceived Usefulness) is weak (β = 0.081), it is not statistically significant (p = 0.285). This shows that the evidence does not support the impact of AI on respondent’s perceptions of usefulness in accounting and financial practices. Finally, AI has a significant positive relationship with reporting and taxes (AI -> Reporting and taxes) (β + = 0.211). This implies AI can automate data collecting, processing, and reporting procedures, resulting in enhanced financial reporting and tax compliance accuracy and timeliness.

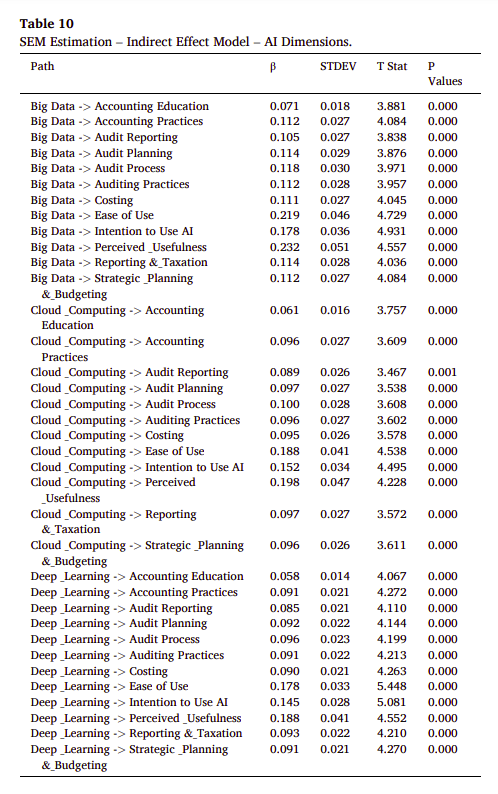

The results in Table 10 exhibit that Big Data, Cloud Computing, and Deep Learning have a statistically significant positive influence on accounting practices and TAM model dimensions. This indicates that using Big Data technologies in accounting education can help students learn more effectively. Also, by embracing Big Data, educational institutions can give students hands-on experience evaluating massive datasets, producing data-driven insights, and comprehending its use in accounting. This is in line with other studies arguing the relevance of incorporating information systems and technology into the accounting curriculum (e.g., Behn et al., 2012; Lawson et al., 2014; Apostolou et al., 2014). Similarly, Sledgianowski et al. (2017) argue that faculty members can actively involve accounting and non-accounting students in accounting learning by leveraging technology and Big Data.

By analyzing cost-related data, optimizing cost allocation, and improving cost forecasting, Deep Learning enhances organizations’ costing practices and decision-making regarding resource allocation. By developing user-friendly interfaces, intelligent automation, and enhanced data visualization, Deep Learning improves the user experience, simplifies complex tasks, and reduces barriers to adoption. The intention to use AI in accounting is positively influenced by Deep Learning, learning serves as a fundamental component of AI technologies, influencing individuals’ perception and acceptance of AI in accounting practices. Individuals perceive Deep Learning as useful in accounting. Deep Learning techniques enhance data analysis, decisionmaking capabilities, and generate valuable insights, thus improving the perceived usefulness of accounting practices. By automating data collection, analysis, and reporting processes, Deep Learning improves the accuracy, timeliness, and compliance of reporting and taxation practices. By providing advanced analytics, forecasting capabilities, and scenario analysis, Deep Learning enhances organizations’ strategic planning and budgeting processes, enabling data-driven decisions, accurate forecasts, and optimized plans and budgets.

[Table 9]

[Table 10]

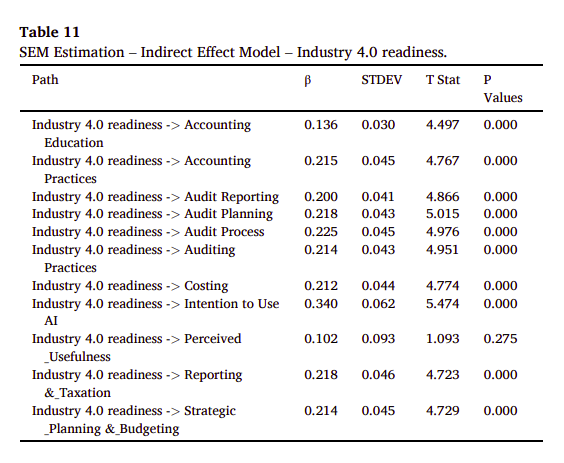

The effect of Industry 4.0

The results in Table 11 reveal that Industry 4.0 readiness have a significant positive impact on various aspects of accounting. In terms of Accounting Education, Industry 4.0 readiness shows a positive relationship. This means that incorporating concepts and tools related to automation, data analytics, and artificial intelligence into accounting curricula, students can develop skills to adapt to technological advancements in the field. Likewise, Industry 4.0 readiness has a positive effect on Accounting Practices, as indicated by a coefficient of 0.215. This indicates that Industry 4.0 readiness, such as automation, data integration, and advanced analytics, improves the efficiency and effectiveness of accounting processes, reducing manual errors and enhancing decision-making capabilities.

Additionally, a positive association was found between Audit Reporting and Industry 4.0 readiness, with a coefficient of 0.200, implying that automation, data analysis, and visualization tools provided by Industry 4.0 technologies enhance the accuracy and efficiency of audit reporting processes, enabling auditors to generate comprehensive and real-time reports. This means that risk assessment, and resource allocation can all be optimized using automation, leading to more accurate and efficient audit plans. Likewise, Industry 4.0 readiness has a significant (p = 0.000) influence on the Audit Process, suggesting that robotic process automation and advanced data analytics improve the efficiency and efficacy of audit operations, allowing auditors to complete their responsibilities more quickly and discover potential risks and difficulties. Thus, auditors can use automation, data analytics, and artificial intelligence to increase the accuracy, efficiency, and effectiveness of auditing operations by acquiring deeper insights, finding patterns, and making educated judgments.

[Table 11]

Industry 4.0 readiness is also positively associated with costing, with a coefficient of 0.212. Its technologies can improve cost estimates, cost allocation, and cost management through automation, real-time data integration, and advanced analytics. Similarly, Industry 4.0 technologies foster an atmosphere conducive to the adoption and use of artificial intelligence in accounting activities, boosting decision-making, automating procedures, and increasing overall efficiency. Further, automation, data integration, and sophisticated analytics improve reporting and taxation procedures’ accuracy, timeliness, and efficiency, hence enhancing overall performance. Eventually, organizations with a higher ambition to use AI are more likely to apply the technology in accounting tasks, such as audit reporting, audit planning, audit processes, costing, reporting and taxation, and strategic planning and budgeting. Firms can use AI tools to automate operations, analyze data more effectively, improve accuracy, and improve decision-making capabilities in various areas (Burritt and Christ, 2016; Fernandez-Caram ´ ´es et al., 2019; Ghobakhloo, 2018; Nagy et al., 2018).

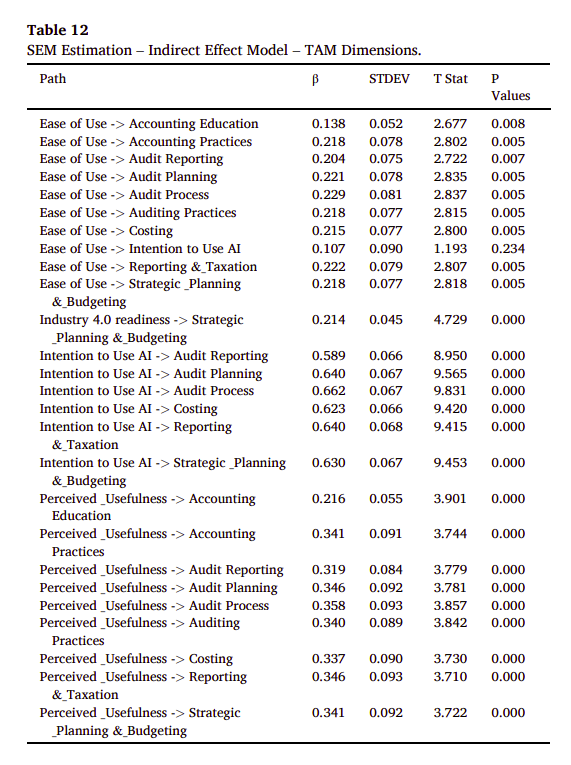

The effect of TAM dimensions

The results in Table 12 show that ease of use, perceived usefulness, and the intention to use AI and Industry 4.0 readiness have a positive influence on Accounting Education, and auditing and accounting practices. The three dimensions exhibit a statistically significant positive effect on audit reporting, planning, and processing. They also reveal a statistically significant positive effect on costing, reporting and taxation, and strategic planning and reporting. Thus, using user-friendly AI technologies in accounting and audit procedures increases productivity and accuracy as these technologies make activities more accessible and less complex for professionals. For example, using AI in audit reporting can streamline the report-generation process, making it easier for auditors to gather and effectively communicate their findings. Furthermore, these solutions streamline the preparation of audit plans, resource allocation, and audit procedure execution, restructuring the planning and execution stages. User-friendly AI solutions can improve the gathering, analysis, and administration of cost-related data in accounting procedures, enhancing accuracy and efficiency. Finally, by providing intuitive interfaces and functionalities, user-friendly AI tools and software help the development of strategic plans and budgets.

[Table 12]

Additional analysis

Subgroup analysis is conducted to assess if there are significant differences in the results attributed to the demographic variables. The results in Appendixes II and III provide analysis of variance and multiple comparisons based on subgroup analysis. Surprisingly, the results reveal that there are significant variations among experience groups (6 years, 6 to 10 years, 11 to 15 years, and >15 years). However, there are significant differences in the majority of the variables based on the job position groups (CPAs, board of directors, accountants, and academicians). This could be due to adaptability and openness to change, role-specific relevance, and uniform exposure across roles. Respondents with varying years of experience may be more accustomed to recent developments, while those with fewer years may be more open to change. Role-specific relevance may also influence perceptions, as professionals across roles may perceive AI’s influence similarly due to its broad applications. It is suggested that the integrating accounting and auditing skills is crucial for achieving positive outcomes and managing risks in AI (Batiz-Lazo ´ and Boyns, 2004). Overall, the findings highlight the importance of personalised interventions or educational activities that recognise nuanced variances in perceptions depending on experience while also recognising the overall alignment of viewpoints across varied professional professions. The rise of AI in the accounting industry has led to a shift from lower-skilled arithmetic roles to higher-skilled roles, highlighting the industry’s resilience and AI’s ability to enhance human capabilities (B´ atiz-Lazo and Boyns, 2004; Ogaluzor, 2019). This transformation has led to the emergence of positions requiring advanced analytical skills, critical thinking, and strategic decision-making. Professionals are now embracing AI tools to provide more insightful financial analysis and strategic advice, creating new career opportunities and specialization. The accounting industry’s growth highlights the need for staff that can adapt to AI technologies, focusing on human skills like creativity, problem-solving, and interpersonal communication.

Discussion and implications

According to the present study’s findings, Big Data technologies enable accountants to efficiently process and analyze huge amounts of data. For instance, accountants can gain important insights, identify patterns and trends, and make data-driven decisions using Big Data analytics, which improves accounting processes. Furthermore, Big Data has an important effect on audit reporting, planning, processes, and procedures. The results indicate that auditors can use Big Data analytics to extract relevant information from massive datasets, uncover potential risks and abnormalities, streamline audit procedures, and improve auditing processes’ accuracy, efficiency, and effectiveness. Big Data also reveals a positive relationship with Costing. This implies that the respondents perceive that big data could be beneficial for business organizations in cost aspects.

Since Big Data analytics provide significant insights and improve decision-making processes, they increase accounting experts’ perceived usefulness. Big Data analytics may also help organizations gain accurate and timely reporting, maintain regulatory compliance, and improve overall reporting and taxation procedures. Hence, the analytics give firms useful visions and predictive capabilities for strategic decisionmaking and budgeting processes. In this sense, organizations may improve forecast accuracy, uncover development possibilities, and optimize resource allocation. Several studies (Brown-Liburd and Vasarhelyi, 2015; Huerta and Jensen, 2017; Salijeni et al., 2019; Sun and Vasarhelyi, 2018; Warren et al., 2015) also indicate that big data can streamline the accounting and auditing tasks, enhance the accuracy and timeliness of reporting, improve the efficiency and effectiveness of the tasks, leading to more efficient and insightful accounting and auditing performance.

It can be also inferred from the results that Big Data technologies add to the usability of accounting systems and applications by simplifying data management operations, providing intuitive visualization and reporting capabilities, and increasing overall user experience. In the same context, the findings confirm that Big Data analytics serve as the cornerstone for accounting AI technologies, giving the essential data for training AI models and producing accurate forecasts. Organizations may develop an atmosphere that encourages the adoption and use of AI in accounting processes by exploiting Big Data. This is consistent with (Brown-Liburd and Vasarhelyi, 2015; Cockcroft and Russell, 2018; Gepp et al., 2018; Salijeni et al., 2019; Sledgianowski et al., 2017; Warren et al., 2015).

With regard to cloud computing, it is exhibited in the results that implementing the technology into accounting education can improve the learning experience by boosting access to materials and tools, creating collaborative learning opportunities, and modeling real-world accounting scenarios. Accountants can benefit from Cloud Computing’s scalable computing resources, remote data storage, and collaborative platforms, which allow them to accomplish jobs more efficiently, work smoothly with team members, and access real-time financial information from anywhere. Auditors also can use Cloud Computing technologies to store and analyze large volumes of audit data, streamline the reporting process, enhance the accuracy and timeliness of audit reports, improve the efficiency and effectiveness of audit planning processes, perform data-intensive tasks, analyze large datasets, and automate certain audit procedures, leading to more efficient and insightful audits.

In the context of Costing, organizations can optimize their costing practices by efficiently processing and analyzing cost-related data through Cloud Computing’s cost-effective computing resources and data storage options. The argument supports (Bianchi and Sousa, 2016; Faccia et al., 2019; Frank et al., 2019; Schumacher et al., 2016). Guan et al. (2020), Issa et al. (2016), Sun and Vasarhelyi (2018) also indicate that cloud computing improves the efficiency and effectiveness of business operations.

The effect of deep learning on accounting education could lead to interpretation that students can develop practical skills and information linked to the application of sophisticated technologies, automate tasks, and receive individualized learning experiences by incorporating Deep Learning techniques into accounting education. Deep Learning also has a positive relationship with Accounting Practices. Deep Learning increases the accuracy, efficiency, and effectiveness of accounting operations by automating repetitive tasks, analyzing massive amounts of data, and discovering patterns or abnormalities in financial data. Deep Learning improves audit reporting, audit planning, the audit process, and auditing practices. Furthermore, Deep Learning algorithms can analyze and interpret audit data, identify risks, and generate more accurate audit reports, thus providing valuable insights to stakeholders and enhancing the overall audit process.

The integration of AI technologies and accounting and auditing expertise is crucial for mitigating risks and achieving beneficial outcomes (Batiz-Lazo ´ and Boyns, 2004). This collaboration improves efficiency and accuracy, while ensuring data security, ethical AI deployment, and regulatory compliance. Accountants play a vital role in ensuring AI applications align with organizational values and avoiding immoral decision-making. This holistic approach highlights the transformative potential of AI in economic institutions and the importance of a harmonious collaboration between AI technology and accounting and auditing skills. Further, the AI governance ecosystem is facing challenges due to insufficient internal control implementation and underutilization of audit activities, particularly in large corporations. Percy et al. (2021) advocate that the present ecosystem is imbalanced, necessitating greater transparency via AI, sufficient documentation, and process formalisation in order to facilitate internal audits and external accreditation processes. In this context, Anderljung et al. (2023) indicate that AI governance involves policies, legislation, and ethical frameworks for responsible AI development and usage. It requires credible information from external sources like audits and third-party research. The ASPIRE framework outlines criteria for effective external scrutiny of border LLMs including access, a searching approach, risk proportionality, independence, resources, and expertise (Anderljung et al., 2023). Accordingly, accounting and finance professionals can help address these issues by improving data governance, enhancing data accuracy, and enhancing risk assessment and management. They also contribute to compliance, performance evaluation, financial visibility, strategic risk management, and a comprehensive approach to governance. Integrating financial specialists into AI governance can provide insights into the financial implications of AI investments, align with budgetary goals, and provide a strategic advantage in navigating uncertainties associated with AI adoption (Anderljung et al., 2023; Percy et al., 2021; Ogaluzor, 2019).

The integration of artificial intelligence (AI) into accounting and auditing processes has raised concerns about job displacement, especially in repetitive tasks (Chen and Wen, 2021; Zhang and Dafoe, 2019). Initially, these concerns were about job losses in physical labor. However, as the industry expanded, new opportunities for higher-skilled professionals emerged, creating a dynamic and knowledge-based accounting sector. AI can automate tasks like math and data entry but also allows professionals to focus on critical thinking, strategic decision-making, and complex problem-solving (Ogaluzor, 2019). This highlights the importance of ongoing professional development and adaptation, as human expertise complements AI capabilities (Ba´tiz-Lazo & Boyns, 2004; Ogaluzor, 2019). Thus, organizations and educational institutions are crucial in preparing professionals for this transition (Zhang and Dafoe, 2019).

Conclusion

The present study has investigated the impact of artificial intelligence, Industry 4.0, and Technology Acceptance Model (TAM) factors on accounting and auditing methods. AI and Industry 4.0 readiness have been used as independent variables, whereas accounting education and auditing and accounting practices have been considered dependent variables. Further, TAM dimensions have been considered as mediating variables that mediate the relationship between AI and Industry 4.0 readiness and accounting and auditing practices. The research has uncovered several significant links between AI, Big Data, Cloud Computing, Deep Learning, perceived ease of use, perceived utility, intention to employ AI, and various areas of accounting and auditing processes. Convenience and snowballing sampling methods have been used to collect the data from various Saudi organizations, and the sample size was determined using various techniques, yielding a final sample of 228 respondents.

The study found a positive relationship between AI and perceived usefulness, implying that AI is considered beneficial for enhancing accounting and auditing methods in Saudi Arabia. The study also concluded that ease of use influences perceived utility and intention to utilize AI, implying that user-friendly AI solutions makes accounting and auditing more efficient and effective. According to the findings, Big Data, Cloud Computing, and Deep Learning have a statistically significant and positive association with accounting and auditing practices. This positive relationship emphasizes the positive role of Big Data, Cloud Computing, and Deep Learning in driving AI adoption in accounting and auditing practices, underlining how these tools promote AI integration and application in accounting and auditing practices.

The study also indicated how perceived ease of use influences AI adoption. Respondents who believe AI is easy to use are more likely to use AI technology in their professional operations. Accordingly, Big Data, Cloud Computing, and Deep Learning have a significant impact on accounting processes because respondents perceive that they streamline audit processes, optimize costing, and enhance decision-making.

The research contributes to the understanding of AI acceptance and use in Saudi accounting and auditing practices. This study sheds light on how these factors interact and influence the adoption and deployment of AI technology in this area. The research also adds to the existing body of knowledge by emphasizing the importance of Big Data, Cloud Computing, and Deep Learning in promoting AI adoption in accounting and auditing procedures. The study emphasizes the importance of these technologies in boosting the capabilities and efficacy of accounting and auditing. Further, this research contributes to a better understanding of the characteristics that allow for the successful integration and use of AI in professional accounting and auditing procedures.

Another contribution of the study is its dealing of the relationship between perceived ease of use and intent to utilize AI. The study emphasizes the importance of user-friendly tools and intuitive AI systems in influencing professionals’ intentions to adopt and employ AI technology. This conclusion implies that efforts to design and implement userfriendly AI systems can have a significant impact on their adoption and acceptance in accounting and auditing operations. Furthermore, the study adds to the body of knowledge by giving implications for practitioners, policymakers, and researchers.

The findings of the current study have implications for policymakers, accountants, auditors, educators, and other professionals. Implementing AI can lead to increased efficiency, accuracy, and decision-making capabilities in certain professional sectors. Therefore, the findings of this study can help firms improve their accounting and auditing operations by leveraging AI technologies, Big Data analytics, Cloud Computing, and Deep Learning tools. Adopting AI allows practitioners to automate mundane activities, decrease human errors, and use advanced analytics to glean important insights from massive amounts of data. This can lead to higher audit quality, more competitiveness, and more useful services for clients. Practitioners can investigate the use of these technologies to efficiently handle and analyze huge amounts of data, improve data security and accessibility via cloud-based platforms, and employ powerful machine learning algorithms for predictive analysis and anomaly detection. The findings of this study can be used by policymakers to create supportive frameworks and regulations that encourage the adoption and integration of AI technology in the accounting and auditing fields. This could include offering financial incentives, encouraging knowledge sharing and collaboration among practitioners, and creating partnerships between industry and academics to support domain-specific AI research and development. Policymakers can also address possible issues connected with AI adoption, such as ethics, data privacy, and cybersecurity, by enacting stringent rules and standards.

The implications are not limited to policymakers; the research implications extend to accounting and auditing researchers. The findings open insights for future research, especially in emerging markets, allowing academics to investigate additional aspects and settings connected to AI adoption, including investigating the importance of business culture, leadership support, and staff training in promoting successful AI integration. Researchers might also investigate the impact of artificial intelligence on specific accounting and auditing functions, such as fraud detection, risk assessment, and financial reporting. Future research on AI’s application in accounting and auditing methods should use qualitative methods like case studies, interviews, and ethnographic approaches to explore the specific challenges faced by professionals in emerging economies. The study also encourages interdisciplinary research collaborations. For example, accounting, computer science, and researchers in other related fields can work together to create novel AI solutions directed to the needs of the accounting and auditing area. Cross-disciplinary study can improve knowledge of AI’s potential in addressing difficult challenges faced by accounting and auditing professionals, thereby contributing to the field’s growth.

Despite the significant findings of the current study, it is important to consider limitations that may impact generalizing the results due to inherent limitations that should be taken into consideration. For example, the findings may not be generalizable globally as the study investigates the perception of the respondents from different culture and business settings. Future research could include a wide range of industries, organizational sizes, culture, and geographical regions in order to capture differences in AI adoption and utilization. Furthermore, the study concentrated on the current state of AI adoption in accounting and auditing practices, despite the fact that the field of AI is continuously growing. Longitudinal studies could be considered in future research to follow updates in AI adoption over time, providing a better understanding of the long-term influence on performance, efficiency, and effectiveness. Moreover, the study explores the benefits and opportunities of AI adoption in accounting and auditing. However, it acknowledges limitations, such as an optimism bias in the survey design and a lack of questions addressing potential downsides. The study calls for a more balanced assessment of AI-related concerns. The ad hoc survey, with a convenience sample of 224, reveals a positivity bias, requiring cautious interpretation. The findings highlight the perceived benefits of AI, but further research is needed to explore potential obstacles and issues for a more comprehensive understanding of AI’s impact on accounting and auditing methods. Moreover, the survey involved participants from various Saudi organizations, but it is important to acknowledge that the sample composition may introduce a level of respondent selection bias. This bias may be influenced by factors such as professional roles and a specific focus on individuals interested in AI technology in accounting and auditing. This highlights the importance of cautious interpretation and generalization of the study’s findings and suggests future research to reduce bias and increase diverse perspectives. Future research endeavours may look into measures to reduce bias and increase the inclusion of varied perspectives within the surveyed community.

The current research focused primarily on the adoption and usage of AI technologies in accounting and auditing operations. It did not, however, go into detail on the obstacles and barriers that businesses may experience during the implementation process. Hence, future research could look into the organizational, technical, and cultural challenges to AI adoption in various sectors. Understanding these issues can provide significant insights and aid companies in developing ways to address problems.

Besides, the present research was limited to large organizations, and the results may not apply to small and medium-sized enterprises (SMEs). Future studies could thus look into the specific obstacles and opportunities that SMEs encounter when adopting and implementing AI technologies in their accounting and auditing practices.

Another area for future investigation is the impact of AI on the accounting and auditing workforce. While the study only briefly mentioned the function of human-machine interaction, more research might look into the specific tasks and responsibilities that may be impacted by AI adoption. Understanding the consequences for job positions, skill needs, and workforce dynamics can help firms manage the transition and ensure that AI technologies are integrated smoothly. Future research also may investigate incorporating qualitative methods like ethnographic studies and surveys to understand the impact of AI adoption in the accounting and auditing industries. Finally, the present study explored the advantages and prospects connected with AI adoption in accounting and auditing. Potential dangers and obstacles, such as cybersecurity threats, data integrity issues, and regulatory compliance, are good backgrounds for future research. Investigating these risks can assist organizations in developing strong policies to mitigate any negative outcomes and ensuring the proper use of AI technologies. To sum up, scholars can improve our grasp of the implications, problems, and prospects of AI adoption in the accounting and auditing domain by addressing these constraints and investigating these future research paths. This knowledge can help practitioners, policymakers, and academics make informed decisions while also supporting the effective and responsible use of artificial intelligence technologies.

Ethical Statement

Not Applicable because the research conducted for this paper did not involve experimentation on animal or human subjects. Ethical considerations and approvals were duly adhered to in the conduct of this research.

CRediT authorship contribution statement

Faozi A. Almaqtari, Abdulwahid Ahmad Hashed Abdullah: Conceptualization, Methodology, Resources, Software, Validation, Visualization, Writing – original draft, Writing – review & editing, Conceived and designed the experiments, Performed the experiments, Analysed and interpreted the data, Contributed reagents, Materials, Analysis tools or data, Wrote the paper. Faozi A. Almaqtari: Formal analysis. Abdulwahid Ahmad Hashed Abdullah: Project administration.

Declaration of Competing Interest